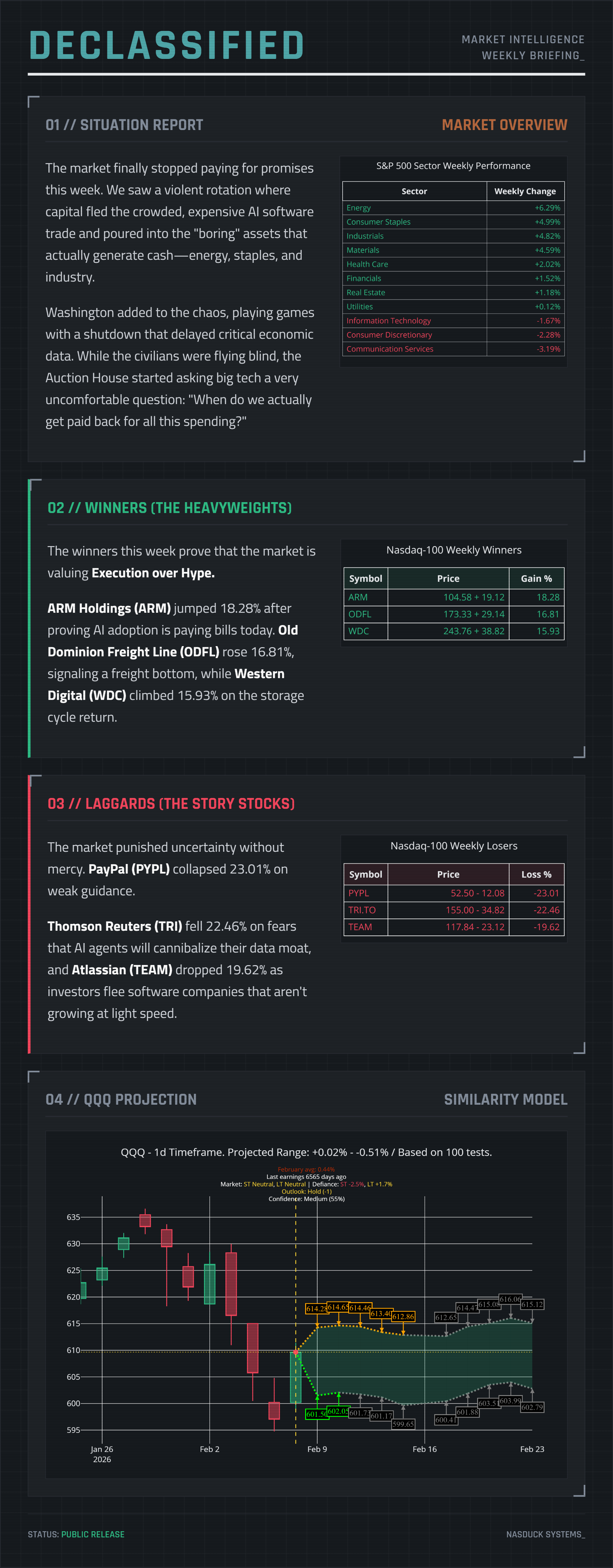

“Kill Shot” Resets Wall Street

Capital is violently rotating out of the “Magnificent Seven”.

📈 LEAD STORY 📉

The Fed Put just expired. Trump’s surprise early nomination of Kevin Warsh was a calculated kill shot that turned Jerome Powell into a ghost with a gavel. The bond market reaction was instant and violent: a Bear Steepener that is currently crushing the present value of high-flying tech stocks while breathing life into forgotten sectors.

Capital is violently rotating out of the Magnificent Seven and into the physical economy—energy, industrials, and regional banks.

I am watching the long end of the yield curve. If you are still using a 2024 playbook on this 2026 battlefield, your portfolio is fighting a war it cannot win. Read on for the new rules of engagement.

QUESTION FOR YOU

With the Warsh Doctrine favoring cash flows and real assets over digital promises, are you finally rotating out of Big Tech, or are you treating this kill shot dip as one last buying opportunity?

█ DECLASSIFIED SECTION █

Read this on our Substack for best experience.

🎧 PODCAST ▰▱

NASDAQ💯 REPORT ▰▱

💸 EARNINGS VS. REALITY ▰▱

🔥 RICK’S HOT TAKE ▰▱

Changing the Rules for Warsh

Think they only replaced a Fed Chair? Think again.

On January 30th, Trump nominated Kevin Warsh to succeed Jerome Powell — four months before Powell’s term even expires. It was a kill shot. Treasury Secretary Scott Bessent has been pitching a “Shadow Fed Chair” strategy since 2024: announce early, hijack the narrative, and turn the sitting Chair into a ghost with a gavel but no power. Powell still runs FOMC meetings through May. But every bond trader on the planet is now pricing Warsh’s words, not Powell’s. The Fed got two bosses saying different things at the same time.

Chaos. By design.

And the intimidation didn’t stop at personnel. The DOJ issued subpoenas over renovation costs at Fed headquarters — a building project. If you think federal prosecutors suddenly care about drywall budgets, I’ve got a bridge to sell you. Senator Tillis and the Senate Banking Committee are now blocking nominees until these “pretextual” probes get resolved. Democrats are calling them sham investigations. Meanwhile, Trump told NBC on February 4th that the Fed Chair should follow his directives because he knows the economy “better than almost anybody” and has “always been good at money.” He admitted Warsh wouldn’t have gotten the job if he’d expressed any desire to raise rates.

Here’s what the market heard: the Fed is now a subordinate agency.

The reaction was instant and brutal. Gold cratered nearly 8% — from record highs near $5,600 to under $4,500. Silver got vaporized, down over 25%. Bitcoin dumped from ~$90,000 to the low $80,000s and later tested $77,000. The era of endless money-printing just got a termination notice. Warsh is a “hard money” guy. He wants positive real rates — meaning your dollars actually hold value. When gold’s insurance premium against currency debasement evaporates, gold crashes. When the liquidity spigot that pumps crypto rallies gets turned off, crypto crashes.

But here’s what most people missed: the stock market rotated. High-valuation tech (your Magnificent Seven) sold off because rising long-term rates crush the present value of future cash flows. Meanwhile, regional banks and small caps rallied — because a steep yield curve is rocket fuel for banks that borrow short and lend long, and rate cuts on the short end directly reduce floating-rate debt costs for small companies.

The bond market told you everything. Short-term yields dropped (pricing in Warsh’s rate cuts). Long-term yields rose (pricing in aggressive Quantitative Tightening — the Fed dumping $6+ trillion in bonds back into the market). That’s a Bear Steepener. And if you don’t know what that means for your portfolio, you need to — because this environment has specific winners and specific losers.

Warsh’s actual philosophy is what I’d call the “Paradoxical Doctrine”: cut rates to help Main Street while shrinking the balance sheet to punish speculation. Lower the price of money. Reduce the quantity of money. He thinks the Fed’s bloated balance sheet has been subsidizing Wall Street’s gambling addiction for fifteen years, and he’s not wrong. He also believes AI is a structural deflationary force — meaning the economy can grow faster without triggering inflation. That gives him intellectual cover to cut rates even if GDP stays hot.

This is a new regime. The “Fed Put” — the assumption that the central bank will rescue your portfolio every time stocks dip — just got its strike price moved way, way lower. If you’re still positioned for the Powell era, you’re bringing a 2024 map to a 2026 battlefield.

Inside the members-only briefing:

The exact sectors and asset classes that quietly win under the Warsh Doctrine — and the ones I refuse to touch

My full scenario framework with probability weights for a soft landing, stagflation, or liquidity accident

How I’d restructure a portfolio right now so the regime change works for you, not against you

If you’re asking “Okay, how do I actually position my money so this Warsh pivot doesn’t blow up my portfolio?”, that’s the playbook I spell out for members.

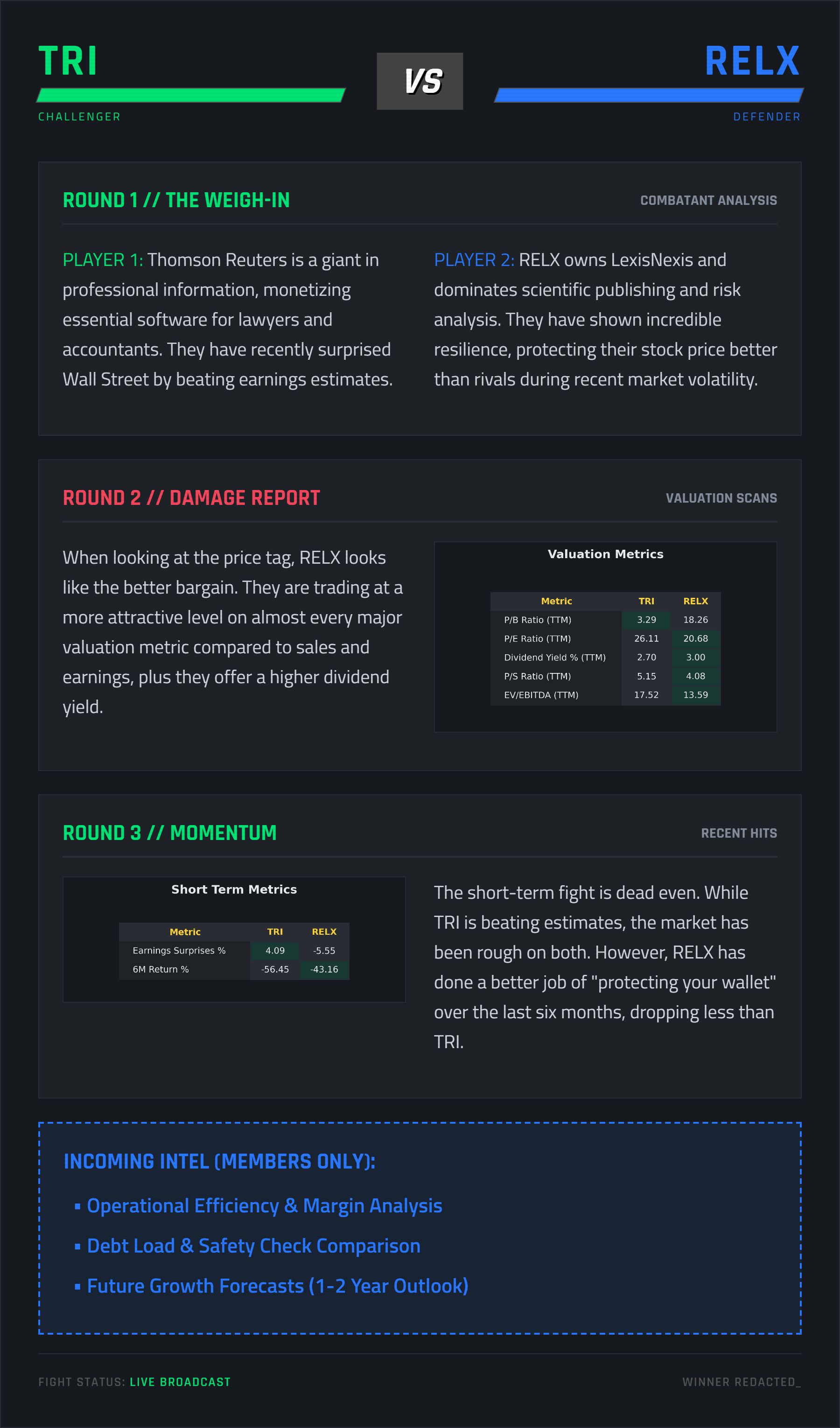

🥊 STOCK DUEL: TRI vs. RELX ▰▱

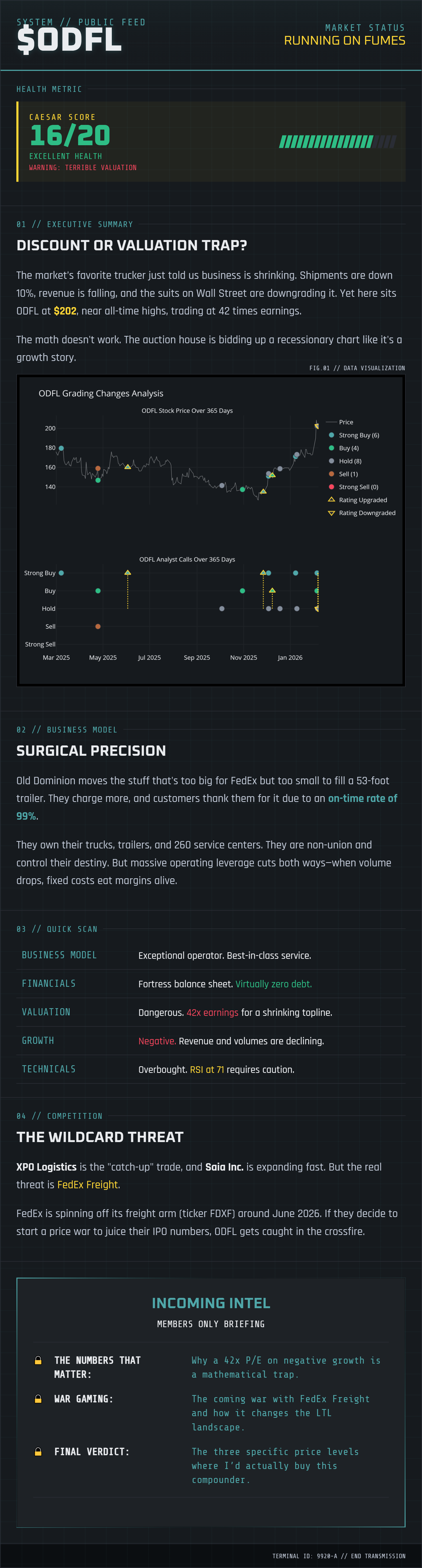

💲ODFL LONG-TERM ▰▱

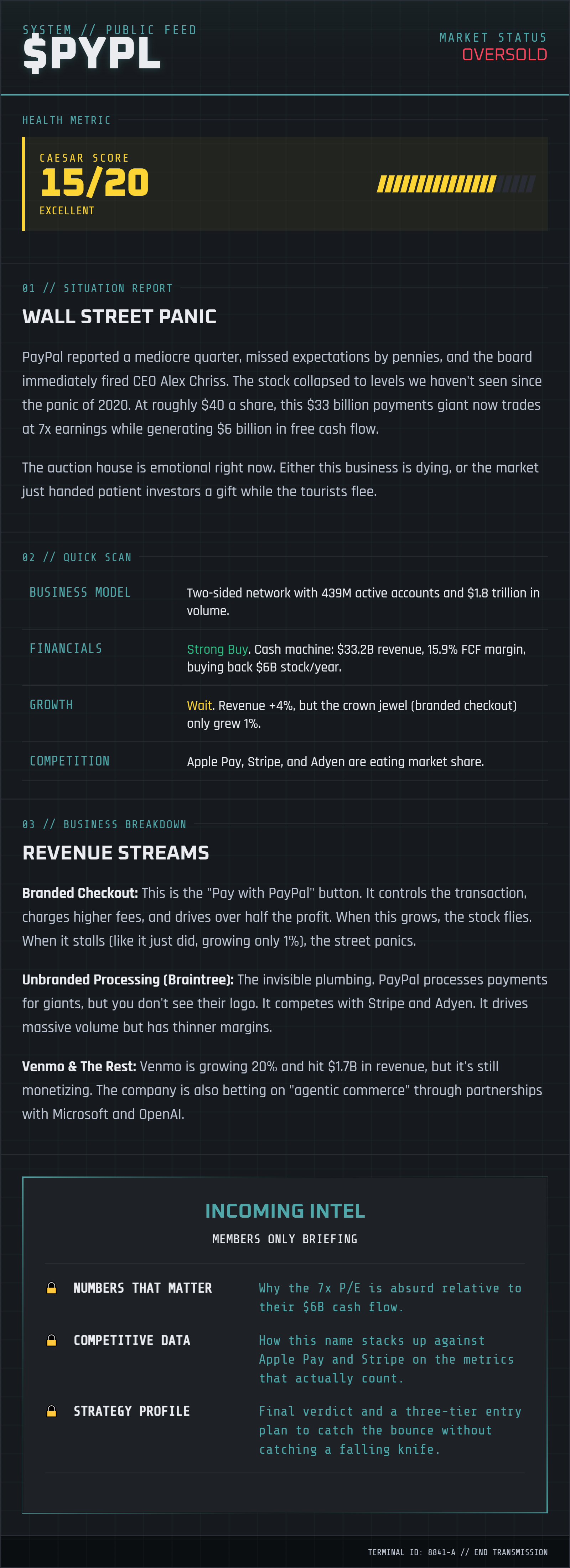

💲PYPL LONG-TERM ▰▱

This post merely reflects its authors’ opinions. This is not financial advice. The stock market involves high risk, so consider your personal situation before investing.